After a car accident in North Carolina, the medical bills show up fast — and from every direction. The ER visit. The ambulance ride. Radiology. The follow-up with your primary care doctor. Physical therapy. Maybe an MRI or a referral to a specialist. Within weeks you’re staring at a stack of bills totaling thousands of dollars and wondering: who’s supposed to pay for all this?

The answer isn’t simple, and that’s by design. The insurance system in North Carolina involves multiple layers — MedPay, health insurance, liens, and subrogation — that all interact in ways that can either help you or leave you holding the bag. I’m a personal injury attorney in Belmont, NC, and before I started representing injured people, I spent years on the insurance defense side. I’ve seen how these billing disputes play out from every angle, and I’m going to break it all down for you.

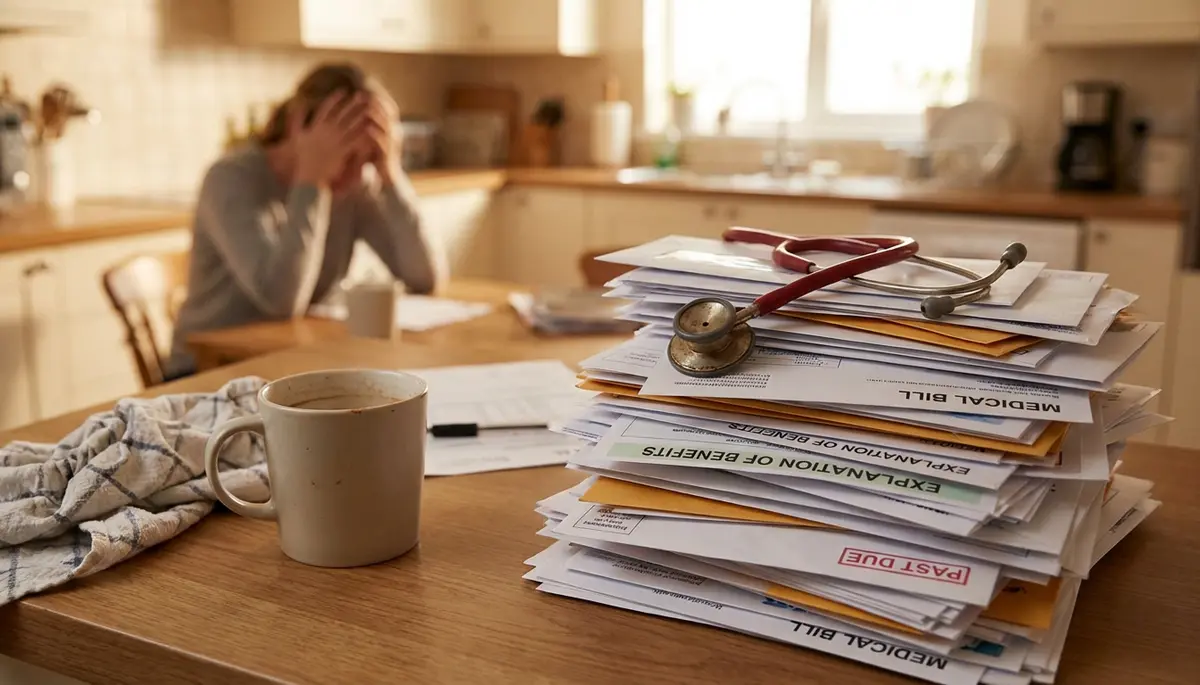

Medical bills after a car accident in NC involve multiple insurance layers — understanding who pays what is the first step to protecting yourself.

North Carolina is a fault state — what that means for your bills

North Carolina is a “fault” state for car accidents. That means the person who caused the accident is financially responsible for the other driver’s injuries and damages. In theory, the at-fault driver’s liability insurance should pay your medical bills.

In practice, it doesn’t work that fast. The at-fault driver’s insurance company isn’t going to start cutting checks to your doctors while you’re still treating. They’ll wait until your case is resolved — either through settlement or a court judgment — before they pay anything. That means someone else has to cover your medical bills in the meantime.

So who pays while you wait? Let’s go through the options.

MedPay: your first line of defense

MedPay (medical payments coverage) is an optional add-on to your own car insurance policy. If you have it, it pays your medical bills regardless of who caused the accident. No deductible. No copay. No waiting for the other driver’s insurance to settle.

In North Carolina, MedPay coverage is typically available in amounts from $1,000 to $10,000, though some policies offer more. It covers:

- Emergency room visits

- Ambulance transport

- Doctor visits related to the accident

- Physical therapy

- Surgery and hospitalization

- Dental work if your teeth were damaged in the crash

Here’s the thing about MedPay that most people don’t know: using it won’t raise your insurance rates. It’s a no-fault coverage, meaning it pays out regardless of who was at fault. There’s no reason not to use it if you have it.

If you’re not sure whether your policy includes MedPay, check your declarations page or call your insurance agent. I recommend every driver in NC carry at least $10,000 in MedPay coverage. It’s cheap — usually just a few dollars per month — and it can be the difference between getting treatment right away and waiting months for the other driver’s insurance to pay.

Health insurance: your second layer of coverage

If your MedPay runs out (or you don’t have it), your regular health insurance picks up the rest. Blue Cross, Aetna, United Healthcare, Medicaid, Medicare — whatever you have. Your health insurance will cover your accident-related medical treatment just like it covers any other medical condition.

There are a couple of things to keep in mind here:

First, you’ll still be responsible for your normal copays, deductibles, and coinsurance amounts. Health insurance doesn’t cover 100% of your bills — the out-of-pocket costs are still yours to manage during the case.

Second — and this is where it gets complicated — your health insurer will probably assert a right to get reimbursed from your settlement. That right is called subrogation, and I’ll explain how it works in a minute.

What if you don’t have health insurance?

This is more common than you’d think, and it creates real problems. Without health insurance or MedPay, you’re looking at paying for accident-related medical care out of pocket — and most people can’t afford that.

There are a few options:

Letters of protection (LOPs): A letter of protection is an agreement between your attorney and your medical provider. The provider agrees to treat you now and wait to get paid from your settlement later. The letter essentially says: “My client was in an accident. I represent them. When we resolve the case, we’ll pay your medical bills from the proceeds.”

LOPs are common in personal injury cases, and many providers in the Charlotte and Gaston County area work on this basis. But providers aren’t required to accept LOPs, and the ones that do are essentially extending credit with the risk that your case might not resolve favorably.

Medicaid: If you qualify based on income, Medicaid will cover your accident-related treatment. Medicaid does have subrogation rights, so they’ll seek reimbursement from your settlement.

Understanding liens on your settlement

A lien is a legal claim against your settlement proceeds. When a medical provider or insurer pays for your accident-related treatment, they may have the right to be reimbursed from whatever money you recover from the at-fault driver.

Here are the most common types of liens in NC car accident cases:

Health insurance subrogation liens

If your health insurance paid your medical bills, they’ll want that money back. This right is usually spelled out in your policy or plan documents. The specifics depend on whether you have an ERISA plan (employer-sponsored) or a private plan. ERISA plans have strong subrogation rights under federal law. Private plans are governed by state law, which can sometimes be more favorable to you.

Medicare and Medicaid liens

If Medicare or Medicaid paid for your treatment, the federal government has a lien on your settlement. These liens are mandatory and enforceable. You cannot ignore them. Medicare’s lien program (called the Medicare Secondary Payer program) is aggressive about recovering money, and failing to satisfy a Medicare lien can create serious legal problems.

Hospital and provider liens

Under North Carolina law (N.C.G.S. 44-49 and 44-50), hospitals and other medical providers can file liens against your personal injury claim for the cost of treatment they provided. These liens must be properly filed to be enforceable — they have to be filed with the Clerk of Superior Court in the county where the treatment was provided.

MedPay subrogation

If your own auto insurance paid MedPay benefits, they may have a right to subrogation as well — meaning they want to be reimbursed from the at-fault driver’s settlement. Whether they actually have that right depends on the language in your policy. Some policies include subrogation clauses for MedPay; others don’t.

Ryan’s Insider Perspective

On the defense side, I saw how liens could eat into a claimant’s recovery. A client would settle for $50,000, but after the attorney fee, case costs, and lien repayments, they’d walk away with a fraction of that. One of the most valuable things a personal injury attorney does is negotiate those liens down — something most people don’t even realize is possible.

Managing medical bills and liens is one of the most complex — and most important — parts of a personal injury case.

How subrogation works (and why it matters to you)

Subrogation is the process by which an insurer who paid your medical bills steps into your shoes and seeks reimbursement from the at-fault driver (or their insurance company). In plain English: your insurer paid your bills, so now they want that money back from the person who caused your injuries.

Here’s how it plays out in a typical case:

- You’re in a car accident caused by another driver

- Your health insurance pays $20,000 in medical bills

- You hire a lawyer and settle with the at-fault driver’s insurance for $75,000

- Your health insurer sends a subrogation notice saying they want their $20,000 back from your settlement

Without negotiation, that $20,000 comes straight out of your pocket. But here’s what most people don’t know: subrogation amounts are almost always negotiable. Your attorney can often reduce the amount owed, sometimes by 30-50% or more. Health insurers would rather get something than risk getting nothing, and a good lawyer knows how to use that leverage.

Under North Carolina’s “made whole” doctrine, your health insurer’s subrogation right may be limited if your settlement doesn’t fully compensate you for your losses. If you haven’t been “made whole,” the insurer shouldn’t be able to recover the full amount. This is an area where having an attorney who understands these rules makes a real difference in how much money you keep.

How to avoid getting stuck with unpaid medical bills

Here’s the practical advice. If you’ve been in a car accident in North Carolina, take these steps to protect yourself from a billing nightmare:

- Use your MedPay first. File the claim with your own auto insurance right away. Get that coverage working for you from day one.

- Use your health insurance. Give your health insurance information to every medical provider. Don’t let them bill the at-fault driver’s auto insurance directly — that creates complications and delays.

- Keep every bill and EOB. Explanation of Benefits statements from your health insurer show what was billed, what was adjusted, and what was paid. You’ll need all of this when it’s time to settle.

- Don’t ignore collection notices. Medical providers don’t care about your personal injury case timeline. If bills go unpaid, they’ll send them to collections. Talk to your attorney about how to manage this.

- Hire a lawyer early. The medical billing side of a personal injury case is one of the most complex parts. An experienced attorney can set up LOPs, manage lien negotiations, and make sure you don’t leave money on the table.

If you want to understand the full timeline of a car accident case, check out my post on how long you have to file a car accident claim in North Carolina. And if you’re wondering what to do right after a crash, read what to do after a car accident in NC.

Frequently asked questions

Do I have to pay medical bills out of my settlement?

Usually, yes — at least partially. If any insurer or provider has a valid lien or subrogation right, those amounts get paid from your settlement proceeds. Your attorney handles these payments at the end of the case and can often negotiate the amounts down before distributing the remaining funds to you.

What if the at-fault driver doesn’t have insurance?

If the other driver is uninsured, you’d file a claim under your own uninsured motorist (UM) coverage — assuming you have it. UM coverage is required to be offered in North Carolina but not required to be purchased. Your MedPay and health insurance would still cover your medical bills in the meantime.

Can medical providers refuse to treat me if I can’t pay upfront?

Emergency rooms are required to treat you under federal EMTALA laws regardless of your ability to pay. For non-emergency follow-up care, providers can and sometimes do require payment or insurance before treating you. A letter of protection from your attorney can solve this problem in many cases.

Will using MedPay increase my car insurance rates?

No. MedPay is a no-fault coverage, which means using it doesn’t count as a claim against your policy for rating purposes. Filing a MedPay claim should not cause your premiums to go up. If your insurer suggests otherwise, push back — or call my office and I’ll help you sort it out.

Drowning in medical bills after a car accident? Let me sort out who owes what — for free.

Find a Car Accident Lawyer Near You

This blog post is for general informational purposes only and does not constitute legal advice. Every case is different, and outcomes depend on the specific facts and circumstances involved. Contact the Law Office of Ryan P. Duffy for a free consultation to discuss your specific situation.